Link: NY Times: Obamacare’s Insurance Mandate Is Unpopular. So Why Not Just Get Rid of It?

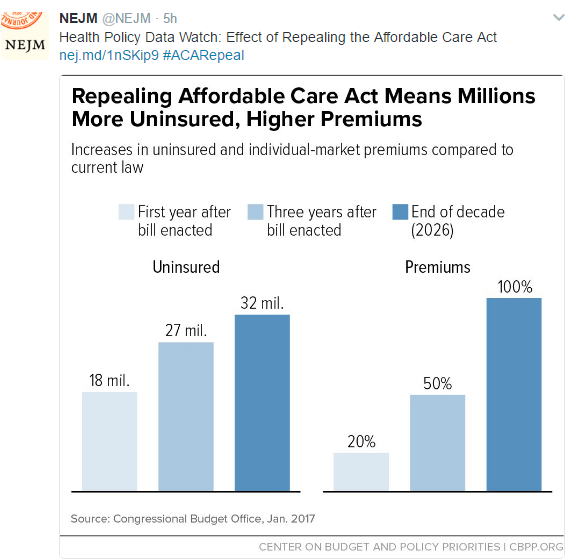

An excerpt: Without the mandate, the C.B.O. has said for years, premiums would spike, and millions fewer Americans would have health insurance. The budget office’s most recent estimate, published last week, said that the ranks of the uninsured would rise by 13 million over 10 years, and that average premiums would be 10 percent higher than under current law.

Here’s an excerpt:

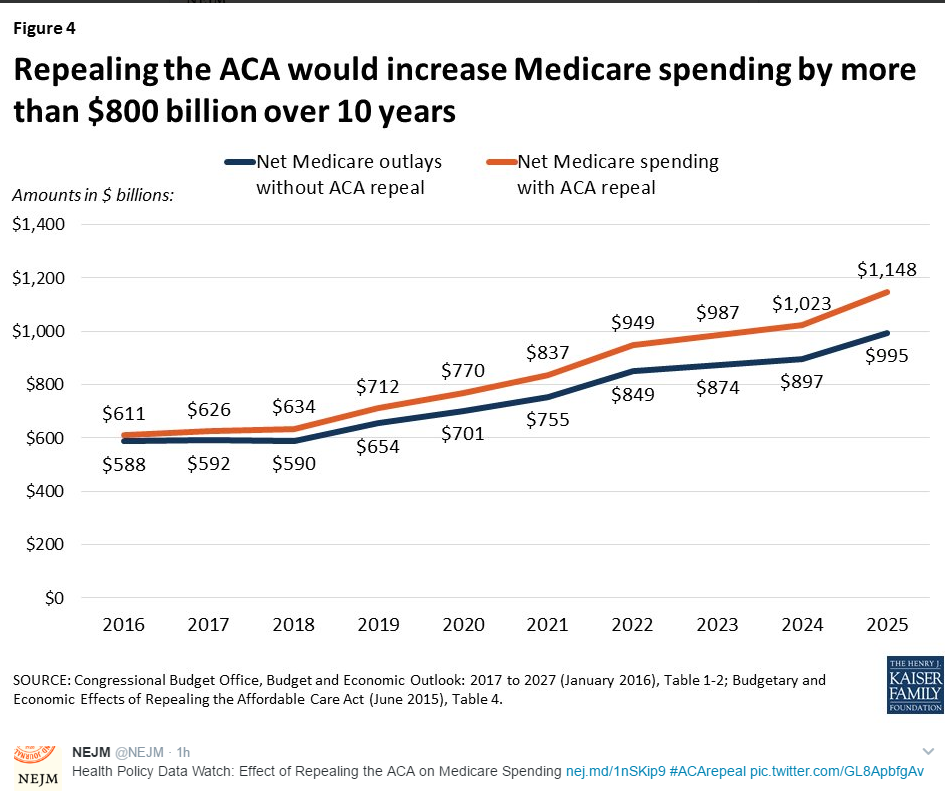

The [AHCA] bill distinguishes itself from the ACA largely by its commitment to regressive redistribution: it would give wealthier Americans more money (mainly through sizable tax cuts) while reducing government support to help low-income Americans afford insurance. Relative to the ACA, premium subsidies for the uninsured would decrease substantially, on average by 40% in 2020 and reaching 50% by 2026.1 Those cuts would fall heavily on lower-income people, with middle- and upper-income Americans receiving higher subsidies.1,3 The ACA’s subsidies to assist low-income persons with deductibles and copayments would be eliminated altogether. By 2026, for a person earning $26,500 a year and buying individual coverage, insurance plans’ actuarial value — which measures the share of costs that plans pay for covered services — would fall from 87% under the ACA to 65% under the GOP plan…

In addition to unified Democratic and significant Republican opposition in Congress and among governors, key stakeholders — including the American Medical Association, the American Hospital Association, and the seniors advocacy group AARP — oppose the bill. Furthermore, as its potential demise draws nearer, the popularity of the ACA, now part of the status quo, is growing. In the Republican imagination, Obamacare has been a disaster. The GOP’s problem is that in reality Obamacare has substantially expanded health coverage, with 20 million Americans gaining insurance. Rolling back the ACA means making insurance less affordable for low-income Americans, increasing the uninsured population, and taking vast funds away from states and medical providers. The GOP health plan neither fully repeals the ACA nor provides a compelling replacement. Instead, in my opinion, it offers only a mirage of reform.

Another analysis indicates significantly higher deductibles are likely under the GOP plan:

Link: Why dedcuctibles would increase under the GOP health plan

In a recent New Yorker article (Jan 23, 2017, pgs 36-45,LINK: “Tell Me Where It Hurts” –thanks to Stan Cohen for this article), Atul Gawande provides a compelling narrative on the ‘heroism’ of incremental care.

He starts his narrative with the story of Bill Haynes who had had severe migraines for four decades, but eventually improved under the care of Elizabeth Loder (John Graham Headache Center). Over the course of four years, her ‘systematic incrementalism had done what nothing else had.’

Dr. Gawande explains that chronic illness is commonplace but “we have been poorly prepared to deal with it. Much of what ails us requires a more patient kind of skill. I was drawn to medicine by the aura of heroism–by the chance to charge in and solve a dangerous problem.”

Despite the appeal of dramatic medical moments, bigger impacts are noted with more subtle care. “States with higher ratios of primary care physicians have lower rates of general mortality, infant mortality, and mortality from specific conditions such as heart disease and stroke.” One of the ways mortality is reduced is getting seen sooner for medical problems. Having a relationship with a physician “has a powerful effect on your willingness to seek care for severe symptoms.”

A parallel narrative in this piece regards the Silver Bridge tragedy in 1967. This bridge which connected Gallipolis, Ohio and Point Pleasant, West Virginia, over the Ohio River, keeled over and resulted in 46 deaths and dozens more who were injured. This tragedy sparked attention towards infrastructure and trying to address problems before a critical collapse occurs. “We will all turn out to have –like the Silver Bridge and the growing crack in its critical steel link–a lurking heart condition or a tumor or a depression or some rare disease that needs to be managed. This is a problem for our healthcare system. It doesn’t put great value on care that takes time to pay off.”

Other points:

My take: Fixing an aging bridge may not be as exciting as building a new one –unless you are the aging bridge or depend on that bridge.

In brief: A recent cross-sectional study (KM Clark et al. J Pediatr 2017; 181: 56-61) showed that breastfeeding at 9 months of age in Chinese infants was associated with iron deficiency anemia.. Iron deficiency can contribute to neurodevelopmental delays in addition to anemia.

My take: In later infancy (after 6 months of age), breastfeeding infants are at increased risk for iron deficiency anemia.

Barack Obama, in a perspective article (BH Obama. NEJM January 6, 2017; DOI: 10.1056/NEJMp1616577), explains the hazards of “repeal and delay.”

Here’s a link to the full text: Repealing the ACA without a Replacement — The Risks to American Health Care

Here’s an excerpt:

Put simply, all our gains are at stake if Congress takes up repealing the health law without an alternative that covers more Americans, improves quality, and makes health care more affordable. That move takes away the opportunity to build on what works and fix what does not. It adds uncertainty to lives of patients, the work of their doctors, and the hospitals and health systems that care for them. And it jeopardizes the improvements in health care that millions of Americans now enjoy.

Congress can take a responsible, bipartisan approach to improving the health care system. This was how we overhauled Medicare’s flawed physician payment system less than 2 years ago. I will applaud legislation that improves Americans’ care, but Republicans should identify improvements and explain their plan from the start — they owe the American people nothing less.

Health care reform isn’t about a nameless, faceless “system.” It’s about the millions of lives at stake — from the cancer survivor who can now take a new job without fear of losing his insurance, to the young person who can stay on her parents’ insurance after college, to the countless Americans who now live healthier lives thanks to the law’s protections. Policymakers should therefore abide by the physician’s oath: “first, do no harm.”

A related article from the LA Times indicates that Aetna misled the public with regard to its reasons for pulling out of several exchanges: Link:U.S. judge finds that Aetna misled the public about its reasons for quitting Obamacare

An excerpt:

The judge’s conclusions about Aetna’s real reasons for pulling out of Obamacare — as opposed to the rationalization the company made in public — are crucial for the debate over the fate of the Affordable Care Act. That’s because the company’s withdrawal has been exploited by Republicans to justify repealing the act. Just last week, House Speaker Paul Ryan (R-Wisc.) cited Aetna’s action on the “Charlie Rose” show, saying that it proved how shaky the exchanges were. ..

Bates found that this rationalization was largely untrue. In fact, he noted, Aetna pulled out of some states and counties that were actually profitable to make a point in its lawsuit defense — and then misled the public about its motivations.

Related blog posts:

A recent NEJM commentary reviews Dr. Tom Price’s congressional record and the implications for his impending appointment to head HHS.

Full Text: Care for the Vulnerable vs Cash for the Powerful –Trump’s Pick for HHS

Here’s an excerpt:

Ostensibly, he emphasizes the importance of making our health care system “more responsive and affordable to meet the needs of America’s patients and those who care for them.”4 But as compared with his predecessors’ actions, Price’s record demonstrates less concern for the sick, the poor, and the health of the public and much greater concern for the economic well-being of their physician caregivers…

Price has sponsored legislation that supports making armor-piercing bullets more accessible and opposing regulations on cigars, and he has voted against regulating tobacco as a drug. His voting record shows long-standing opposition to policies aimed at improving access to care for the most vulnerable Americans. In 2007–2008, during the presidency of George W. Bush, he was one of only 47 representatives to vote against the Domenici–Wellstone Mental Health Parity and Addiction Equity Act, which improved coverage for mental health care in private insurance plans. He also voted against funding for combating AIDS, malaria, and tuberculosis; against expansion of the State Children’s Health Insurance Program; and in favor of allowing hospitals to turn away Medicaid and Medicare patients seeking nonemergency care if they could not afford copayments.

Price favors converting Medicare to a premium-support system and changing the structure of Medicaid to a block grant — policy options that shift financial risk from the federal government to vulnerable populations.

My take: I’m worried that patients who need even basic care may not receive it if the affordable care act is repealed without a backup plan in place.

Related NY Times article discusses Dr. Price: Trump’s Health Secretary Pick Leaves Nation’s Doctors Divided The article discusses the AMA’s endorsement of Dr. Price and how many physicians have countered that the AMA does not speak for them.

Not yet according to a recent commentary: BD Sommers. NEJM 2016; 375: 201-3. The graph below provides some perspective. In addition, the author cautions those who have voiced early alarm bells regarding upcoming rates. He notes the same alarms have been raised in the previous 2 years. Though, he notes, “there are reasons to suspect that marketplace premium growth for 2017 will exceed this year’s levels. Two of the law’s provisions designed to reduce financial risk to insurers in the new markets expire after 2016 — the risk corridor and reinsurance provisions…the country’s continued emergence from the aftermath of the Great Recession may well spur increasing rates of health care inflation for the general population, as well as for the ACA exchanges”

“Premium growth — even when it does reach into the double-digit range that sparks such substantial media attention — is a policy challenge to be examined and addressed and is also part of the general historical pattern that precedes the ACA.” Those who argue “the law as a whole should be scrapped ignore the devastating effect that repeal would have on the estimated 20 million Americans who have thus far gained insurance under the law.”

My take (from commentary): “Regardless of what ends up happening this year, it seems likely that next spring will bring renewed claims that the sky is falling — when experience should make clear that it isn’t.”

A recent commentary (NEJM 2015; 372: 695-98) explains how information provided on healthcare exchanges influences choices on coverage and what types of modifications could help improve these decisions.

Current plans are categorized as Bronze, Silver and Gold based on monthly premiums and out-of-pocket expenses (Related link: Understanding Plans on Healthcare.gov). Gold plans are characterized by higher monthly premiums and lower out-of-pocket expenses. However, the authors sampled a group of people. They found that plans that are labeled as “gold” were preferred by the majority whether the plans had higher monthly premiums and lower out-of-pocket expenses or the reverse (low monthly premiums and higher out-of-pocket expenses). Rather than using “gold,'” “silver,” or “bronze,” their recommendation would be to provide more practical information by providing estimates of annual costs with best-case and worst-case scenarios.

On many exchanges, the plans are listed by order of lowest monthly premiums to highest monthly premiums. “When people make choices, they often settle for options at the top of a menu…for example, all else being equal, politicians listed at the top of ballots receive more votes than those whose names appear lower on the list.” Also, using monthly premium differences rather than weekly premium differences also influences choices. Thus, even the innocuous design of a website, could adversely influence the selection of the best plan for a given participant.

Bottomline: If the affordable care act and health exchanges are not eliminated, improving the presentation of information could help many participants get the health coverage that actually meets their needs.

Related blog posts:

A recent succinct commentary describes the ~20 million people who gained coverage as a result of the Affordable Care Act/Obamacare; the exact number who were uninsured prior is not known. While the article provides a clearer picture of this expansion, it also makes the point that there are many issues that need to be addressed including cost containment. Other subjects:

Here is the link –the entire report is worth a read: ACA -20 million Americans

Here is an excerpt:

Taking all existing coverage expansions together, we estimate that 20 million Americans have gained coverage as of May 1 under the ACA (Figure 3 Categories of Expanded Health Insurance Coverage under the Affordable Care Act (ACA).). We do not know yet exactly how many of these people were previously uninsured, but it seems certain that many were. Recent national surveys seem to confirm this presumption. The CBO projects that the law will decrease the number of uninsured people by 12 million this year and by 26 million by 2017. Early polling data from Gallup, RAND, and the Urban Institute indicate that the number of uninsured people may have already declined by 5 million to 9 million and that the proportion of U.S. adults lacking insurance has fallen from 18% in the third quarter of 2013 to 13.4% in May 2014.

However, these surveys may underestimate total gains, since some were fielded before the late March enrollment surge and do not include children. With continuing enrollment through individual marketplaces, Medicaid, and SHOP, the numbers of Americans gaining insurance for the first time — or insurance that is better in quality or more affordable than their previous policy — will total in the many tens of millions.

As we look to the future of the coverage provisions of the ACA and their effect on the U.S. health care system, several observations seem justified. First, as the number of individuals benefiting from the law grows, its wholesale repeal will grow less likely, although the law could still be importantly modified in the future.

Second, experience with the ACA will vary enormously among states. Those deciding not to expand Medicaid will benefit far less from the law, and since many of these states have high rates of uninsured residents and lower health status, the ACA may have the paradoxical effect of increasing disparities across regions, even as it reduces disparities between previously insured and uninsured Americans as a whole.17

Third, the sustainability of the coverage expansions will depend to a great extent on the ability to control the overall costs of care in the United States. Otherwise, premiums will become increasingly unaffordable for consumers, employers, and the federal government. Insurers who seek to control those costs through increasingly narrow provider networks across all U.S. insurance markets may ultimately leave Americans less satisfied with their health care. Developing and spreading innovative approaches to health care delivery that provide greater quality at lower cost is the next great challenge facing the nation.